As expected by most investors, the Federal Reserve raised its target federal funds rate by 0.25 percent on 16th December, the first such hike since 2006. A priori not a good news for African markets where the main concern could be an acceleration of capital outflows and a return of money to the US. The rate hikes further strengthening the US dollar could cause a spill over effect and potentially exacerbate the emerging market currency turmoil.

Currencies in Kenya, Uganda, and Ghana were mostly unchanged and are expected to remain this way next week. Moreover, African central banks have stated they are ready to defend their economies as the era of low US interest rates come to an end.

The real question is to which extend the long-anticipated rate hike is already priced in? Plunging commodity prices and lower demand from China have already put pressure on Nigeria’s naira and South Africa’s rand especially. The key here would be to look at countries with high current account deficit, private sector credit growth and high levels of foreign debt.

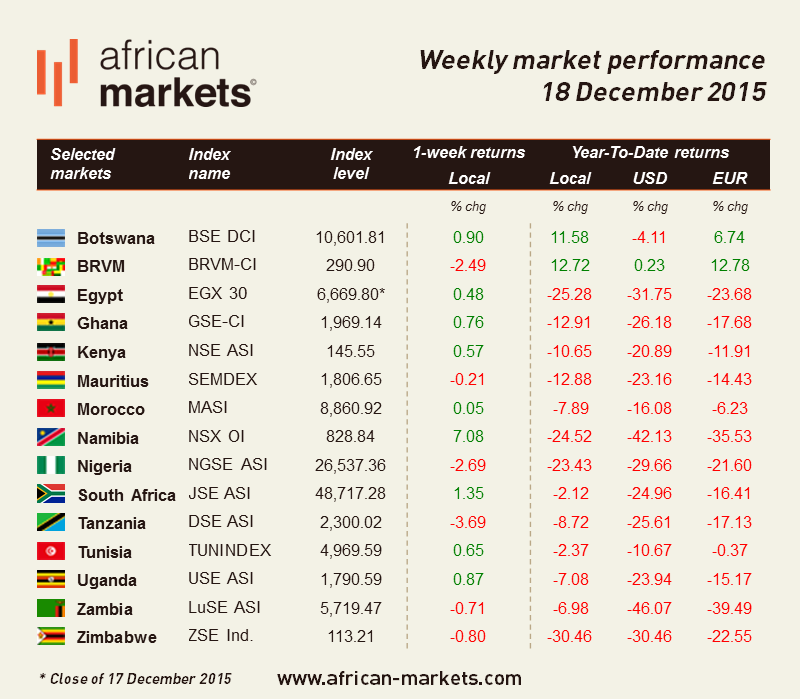

But let’s not get ahead of ourselves, changes to interest rates can take a few months to feed through into the real economy, so let us look at what happened on the African markets this week. One may say that the impact has not been too dramatic…yet?

African markets somewhat showed the same mixed trends this week; same game different players. BRVM declined further 2.49% to close the week at 290.90. A similar declining trends was witnessed on the SEMDEX (-0.21%), NGSE ASI (-2.69%), DSE ASI (-3.69%) despite positive navigating on positive territories last week, LuSE ASI (-0.71%) and the ZSE Ind (-0.80%).

In Nigeria, the naira tumbled to 269 against the United States dollar at the parallel market on Wednesday as the Central Bank of Nigeria started rationing the greenback to Bureaux De Change operators in its weekly foreign exchange sale. On a brighter side, Nigerian OPEC-secretary stated Global crude oil prices at seven-year lows will not continue and could rise in as little as a year. As far as Tanzania is concerned, let us hope that President Magufuli’s dismissed of the head of the government’s for failing to tackle corruption will put the country back on track.

Significant improvements versus last week are to be highlighted on the EGX30 (+0.48%), the GSE-CI (+0.76%), the MASI (+0.05%), the NSX OI (+7.08%) and the JSE ASI (+1.35%). Despite earlier announcement in the week that the government is lowering its ceiling on domestic steel prices by EGP 25-350/ton weighing on the EGX30, the index ended the week on a positive note. The Egyptian positive performance is mostly explained by CIB’s acceptance of OTMT’s USD 128m bid to acquire CIB’s investment subsidiary, CI Capital.

Finally, South African stocks rose to a more than one-week high on Thursday after the United States raised interest rates but a stronger dollar weighed on the battered rand. Furthermore, the market seems to have found relief on Zuma’s Finance Minister U-turn, with Gordhan returning to his functions. Both banks and ZAR on the mend, recovered less than half of last week’s losses.

")