")

The sector outlook for Tunisia's banks in 2019 is negative, reflecting the prospect of continued tight liquidity, rising funding costs and weak economic activity, Fitch Ratings says in an Outlook Report on banking in francophone African countries.

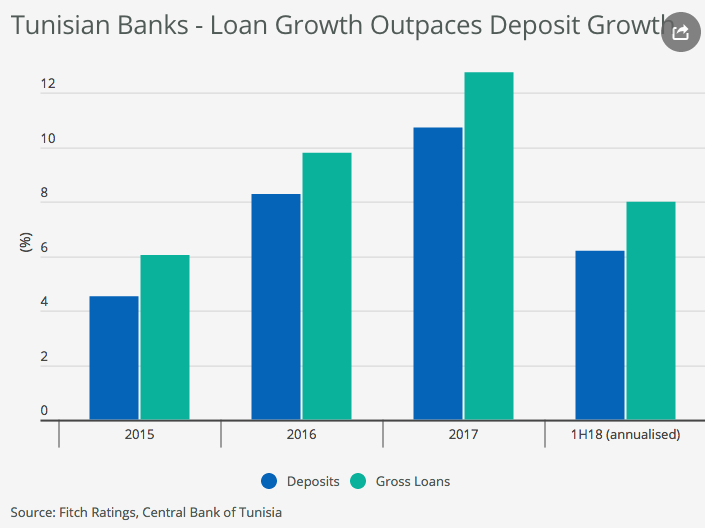

Tight liquidity is the most pressing problem for Tunisian banks and is unlikely to ease significantly in 2019. Customer deposits, the main source of bank funding in the country, are not keeping pace with loan growth and the banking sector's loan/deposit ratio is creeping up (end-June 2018: 131%).

The Central Bank of Tunisia is introducing a limit of 120% on banks' loans/deposits ratios from December 2018, which should slow loan growth and free up some liquidity. But it will not address the problem of modest deposit inflows due to weak public confidence in banks, high inflation and fears of further depreciation of the dinar.

Many banks depend on the central bank for funding. Over 40% of securities held by the sector are pledged to the central bank, and central bank lines were equivalent to about 13% of sector assets at end-1H18. The central bank is keen to reduce this dependence, which is likely to increase pressure on liquidity.

Tunisian banks are exposed to further interest-rate rises. Lending rates are capped, while funding costs could increase as bond issuance becomes more expensive and remunerated deposit rates rise (although the prevalence of non-remunerated deposits softens the impact). The central bank rate has risen to 6.75% from 4.25% since end-1Q17. Lending rates are subject to a cap, the "taux excessif global", of 12.3%. We expect this to be raised in 2019, but we do not expect the increase to keep pace with central bank rate rises.

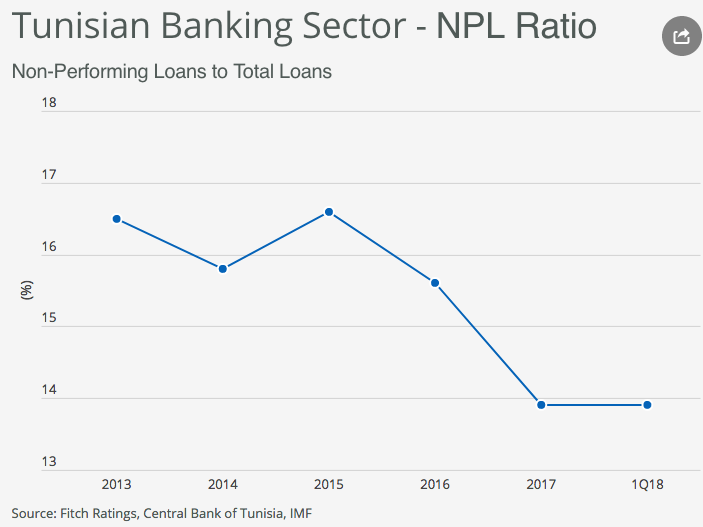

The Tunisian banking sector's ratio of non-performing loans to total loans is high by international standards, and improvements since 2015 could reverse in 2019 due to strains on the economy and business environment. The central bank's efforts to restrict credit could trigger a rise in impaired loans as borrowers find they are unable to roll over loans, and potential interest-rate rises could make it more difficult to service debt. The riskiest sectors are consumer lending, hotels and real estate.

Bank reform in Tunisia, undertaken in conjunction with the IMF, remains slow. There will be new prudential capital requirements in 2019 to capture some aspects of market risk. But it is likely to be several years before Tunisian banking supervision reaches a level that would meaningfully improve banks' credit quality.

Link to Fitch Ratings' Report(s): Fitch Ratings 2019 Outlook: Francophone African Banks