Tunisian banks face a steep rise in credit losses over the next 12 months as borrowers' debt-servicing capacity weakens due to the recent ending of support measures put in place amid the coronavirus pandemic, Fitch Ratings says in a new report. Reduced profitability could pressure already-thin capital buffers, particularly at banks with weaker core profitability. Ratings could be downgraded for banks whose financial metrics deteriorate beyond our baseline expectations.

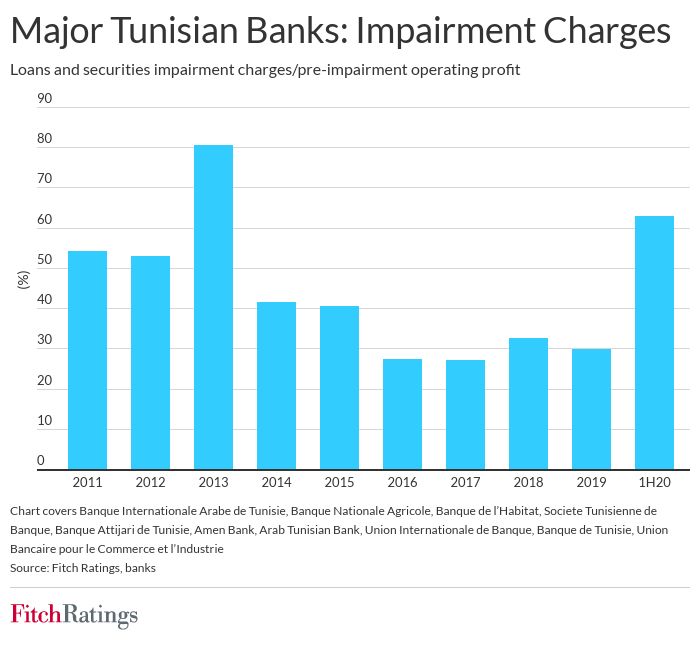

Most major banks had modest increases in loans and securities impairment charges in 1H20, reflecting the mitigating effects of debt relief and regulatory forbearance. The ratio of impairment charges to pre-impairment operating profit rose to 62.9% for our sample of major banks in aggregate, from 29.9% in 2019. However, most of the increase was attributable to one bank, Union Internationale de Banques, including a sharp fall in pre-impairment operating profit and a likely more conservative approach to provisioning, in line with its parent bank, Societe Generale.

We expect the ratio of impairment charges to pre-impairment operating profit to increase in 2021, potentially approaching the peak of 2013 amid social unrest in the aftermath of the Arab Spring. The winding-up of debt relief in September will expose many borrowers to cash flow pressures, particularly those hard hit by the pandemic's impact on tourism, hospitality and exports. Moreover, Tunisian banks' move to IFRS 9 from end-FY2021 is likely to weaken reported asset-quality metrics, and require additional provisioning given the use of forward-looking information in their models.

Fitch expects Tunisia's economy to grow by 4.5% in 2021. But there are downside risks given social tensions, political instability and the uncertainty over the duration and possible tightening of measures taken by the authorities to counter a resurgence in coronavirus infections.

Report "Major Tunisian Banks: 1H20 Results".