")

")

USD denominated Eurobonds have become the darling of the African investor. Nigeria and Ghana are amongst the most popular Eurobonds requested. Nigeria with a low 34.98% debt to GDP ratio offers strong yields with comparatively low risk to capital.

Ghana offers extremely high yields alongside a torrid 78% debt to GDP ratio (March 2022) from 80.1% in December 2021. There are genuine indicators that the economy is on the rebound, but the Sovereign is yet to convince the international markets as the hard sell off within Ghana Eurobond’s persists.

Eurobonds have become the haven asset class for the local investor as global surging inflation seeks to eradicate any real return from local currency assets. Present yields upwards of 20% on 4-to-5-year Ghana risk is attractive in the face of quite serious headwinds.

The Economy

The Ghanaian economy had already been facing fiscal debt challenges since 2014 to which the global pandemic provided an unwelcome catalyst as capital expenditure grew.

The Government in September 2021 laid down a fiscal deficit target of 7.4% to which the international markets deemed over ambitious and unlikely to be achieved. The sell-off made very clear the opinions of the international investors. The markets sought a strong fiscal plan to determine whether the sovereign was indeed back on track.

The Downgrade

Moody’s Ratings, on 4th February 2022, downgraded Ghana’s Long-Term Issuer and Senior unsecured bond Ratings from B3 to Caa1 adding more fuel to an increasing volatile situation.

The E-levy and Budget cuts

Following months of uncertainty the finance minister had some good news for the investor, the e-levy. The levy is projected to rake in approximately $1 bn dollar of revenue to support the country’s fiscal position. Moreover, 30% expenditure cuts were also announced in the budget for 2022. The levy was the ‘silver bullet’ and upon the legislation passing a welcome bounce to Ghana Eurobond prices. The international market awaits news of the implementation and the actual revenue numbers.

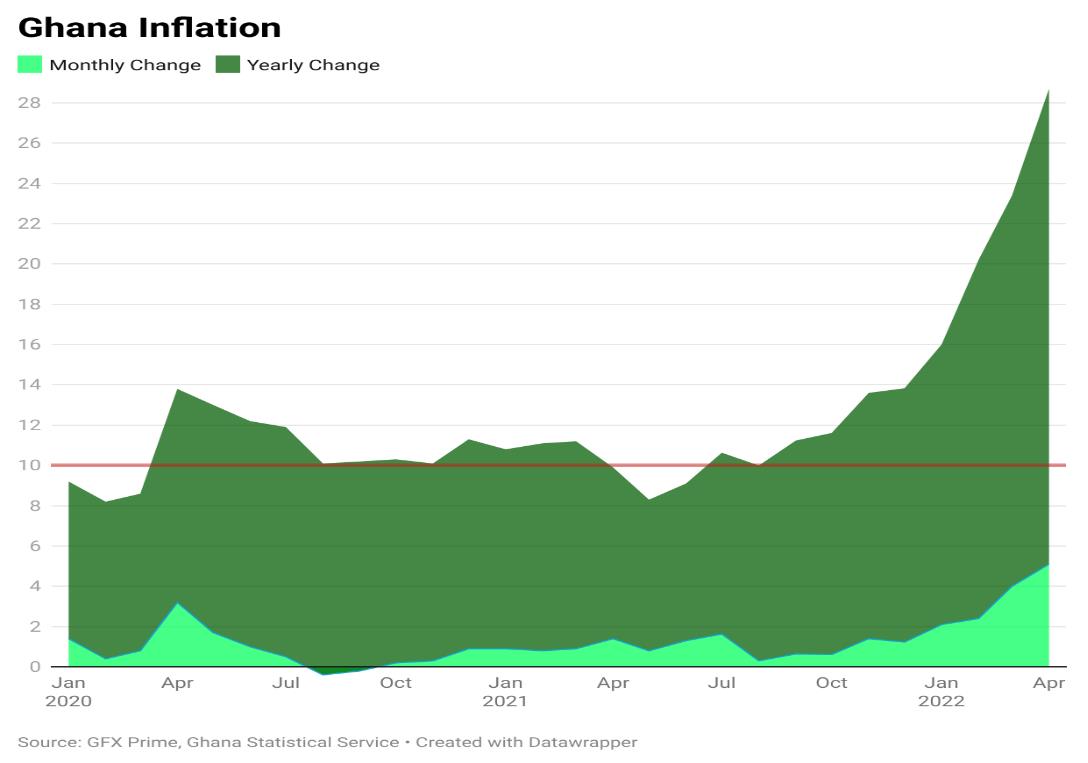

Inflation

Surging global inflation was another hit the sovereign had to react to. The Russian invasion of Ukraine sending commodity prices higher and most recently China’s zero Covid policy locking down Shanghai has added to supply chain woes. The inflation number of 23.6% came in double the Bank of Ghana’s target The Ghana cedi in its free-fall, depreciated by 18.5% in the last four months. A 250bps policy rate hike by Bank of Ghana in March kept exchange rate at a resistance level of GHS 8 against the US dollar slowing down the rate of depreciation. We expect the new 200bps hike to stabilize the cedi further against the dollar.

Positive Indicators

The situation is certainly not as dire. Ghana recorded an annual growth rate of 5.4% and a 7% in the fourth quarter of 2021 beating the forecasts of the central bank and the international monetary fund.

The Reserve

The Bank of Ghana’s net reserves is currently at $4.6bn affording Ghana breathing space to get the ‘fiscal house’ in order, bringing debt to a sustainable level.

Our Opinion

The local investor must now see the sovereign’s current woes as an opportunity. A little too volatile to day trade but a good time to pick up risk across the Ghana Eurobond curve if determined to hold to maturity.

In our estimation the sovereign can continue to service international debt deep into 2024. If access continues to be blocked from international markets, then perhaps the international investor will be eagerly hoping for news of IMF intervention.