")

Markets ended the month on a pretty positive note, with most markets under our coverage closing on positive territory.

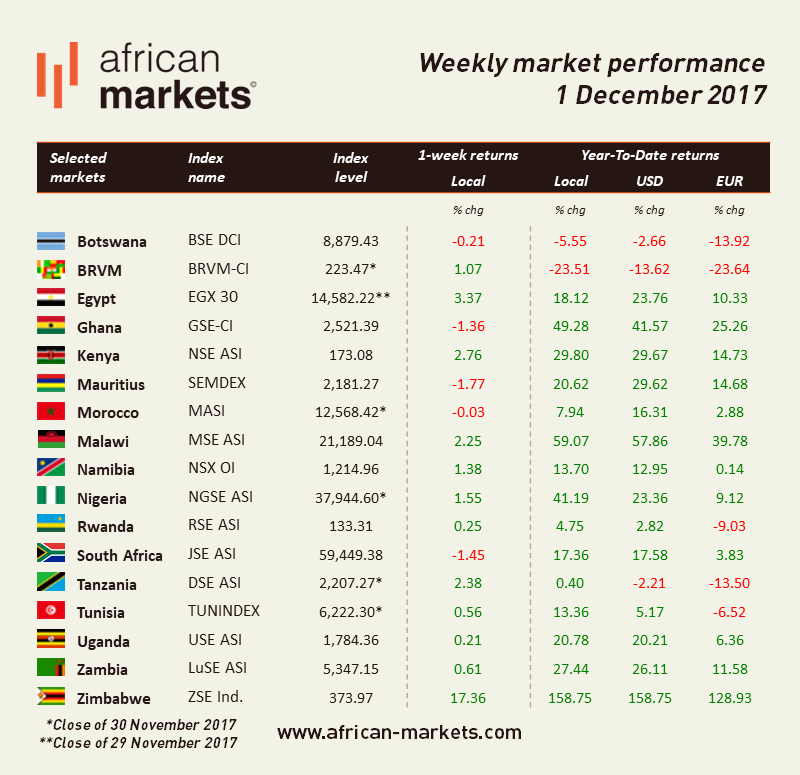

The NSE surged 2.76% as Uhuru Kenyatta was sworn in for his second term after the Supreme court upheld Kenyatta’s victory. This somewhat reassured the market as this could mean the end of months of political turmoil following controversial elections.

The JSE lost 1.45%. The market reaction to the downgrade was relatively mute this week pointing to the fact that much of this was already expected by investors and in the price. Besides, sentiment towards December elections is turning more positive as it is more and more believed that South Africa’s Deputy President Cyril Ramaphosa will win the race to become the next leader of the ruling African National Congress (ANC). Ramaphosa is seen as more business-friendly candidate compared to her opponent Dlamini-Zuma.Now the question to ask is who benefits from the crime? So far bank stocks have proven highly resilient and have taken advantage of a rising rand. As they are highly capitalised they have been able to absorb shocks and on top of that they are cheap. However, the JSE was dragged down by a a global sell-off in technology shares. Naspers which represents more than 20% of the JSE's market value lost 3%. Finally, the firmer rand did not help the performance.

In Zimbabwe, new president Emmerson Mnangagwa appointed his cabinet this week. Among the different appointments, he named Patrick Chinamasa as finance minister, Air Marshal Perrance Shiri land minister and Major General Sibusiso Moyo foreign minister. He also appointed several individuals who served under Mugabe which created some disappointment as bigger change was anticipated by the market. Hence the ZSE rallied this week almost at recouping last week’s performance as concerns increased about the real impact of the new presidency. The ZSE Ind. gained 17.36%.

Nigeria’s got its mojo back as the National Bureau of Statistic published new data on the state of the economy. According to the NBS, capital imports reached over $4 bn in Q3 which represents the first quarterly growth since 2015, just before the economy fell into a recession. The growth was mainly driven by portfolio and other investments. This comes as Nigeria has started its second quarter of recovery. Nigeria’s economy grew 1.4% year-on-year in Q3. The NGSE gained 1.55%.

The EGX gained 3.37% reaching 14,582.22 points, its highest level since September 2017. On Tuesday, the Central Bank of Egypt (CBE) removed caps on foreign-currency deposits and withdrawals for importers of non-essential goods.