")

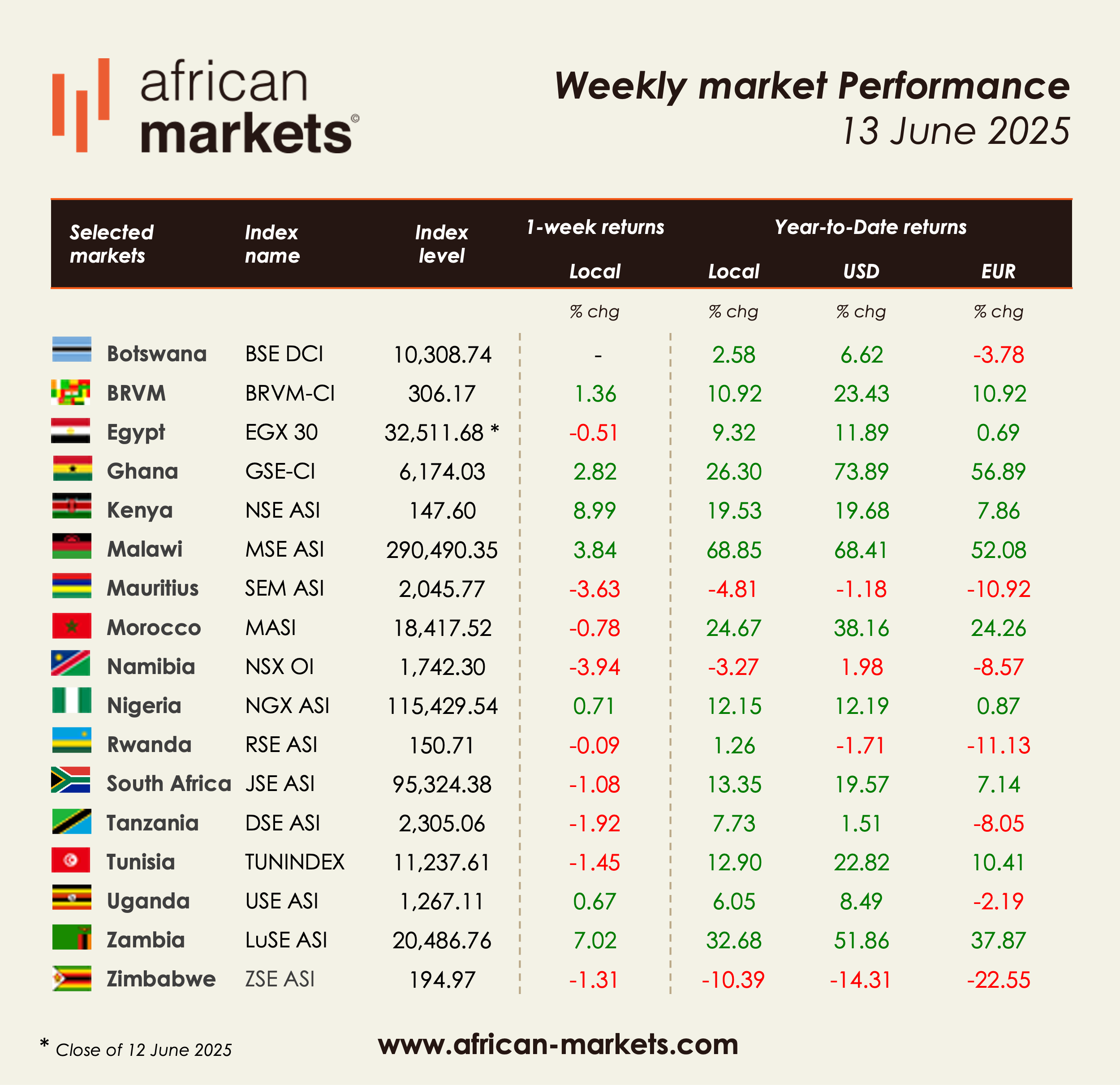

African stock markets showed mixed performances this week, reflecting the continent’s highly localized investment dynamics. While some indices rallied strongly, others faced sharp corrections or continued weakness, highlighting selective investor sentiment.

Top Weekly Gainers: Kenya, Malawi, and Ghana Lead the Charge

Nairobi Securities Exchange (NSE) posted the best weekly gain with a solid +8.99%, driven by broad-based rallies in banking and industrial stocks. Key contributors included Kenya Power (+4.06%), Co-operative Bank (+3.41%), and Kenya Airways (+3.32%), as optimism returns around potential macroeconomic stabilization.

In Malawi, the MSE gained +3.84%, maintaining its remarkable momentum with a +68.85% YTD, bolstered by continued strength in NBS Bank (+32.11% YTD) and FMB Capital (+12.98% YTD).

Ghana’s GSE also performed strongly (+2.82% this week, +26.30% YTD) with notable gains in:

- SIC Insurance (+108%)

- GCB Bank (+35.05%)

- Ecobank Ghana (+31.50%)

- Fan Milk (+12.16%)

The rally suggests sustained investor confidence in selected counters, despite ongoing macro challenges.

Nigeria: Steady Rebound in Financials and Consumer Stocks

The NGX All-Share Index advanced +0.71% this week, buoyed by positive sentiment in financials and consumer names. Several stocks posted double-digit weekly returns:

- Stanbic IBTC Holdings (+9.98%)

- Fidson Healthcare (+9.87%)

- Ellah Lakes (+9.90%)

- BUA Cement (+7.53%)

- Oando (+9.35%)

- Cadbury Nigeria (+5.13%)

However, the market remains volatile, with some notable laggards including John Holt (-18.42%), Conoil (-9.99%), and Northern Nigeria Flour Mills (-10%), emphasizing the importance of selectivity.

On the downside: Mauritius, Namibia, and Zimbabwe face headwinds

The Stock Exchange of Mauritius (SEM) dropped -3.63%, hit by sharp declines in Tropical Paradise (-17.95%), Sun Limited (-13.85%), and Terra Mauricia (-11.36%), likely due to softer tourism-related demand.

Namibia fell -3.94%, extending its year-to-date decline (-3.27% YTD), while Zimbabwe experienced multiple steep losses with Nampak (-24.98%), Willdale (-20.63%), Hippo Valley (-12.86%), and Seed Co (-12.03%) leading the drop. The ZSE remains one of the worst performers YTD in USD terms (-14.31% YTD).

YTD Snapshot: Malawi Still Dominates, Ghana Holds Strong

Despite short-term volatility, year-to-date performance remains robust in several key markets:

- Malawi: +68.85% YTD (Africa's top performer)

- Ghana: +26.30% YTD

- Morocco: +24.67% YTD

- Zambia: +32.68% YTD

Also worth noting is West Africa’s BRVM index (+10.92% YTD, +1.36% this week), with standout stocks including PALMCI (+20.38% YTD), Servair Abidjan (+10.84%), and CFAO Motors CI (+7.09%).

Conclusion: A Fragmented Landscape with Selective Opportunities

This week reaffirms the highly fragmented nature of African equity markets. Investors continue to reward strong fundamentals, especially in financials, agri-business, and consumer sectors. In such an environment, stock picking remains crucial, with a growing divergence between outperformers and structurally challenged names.