")

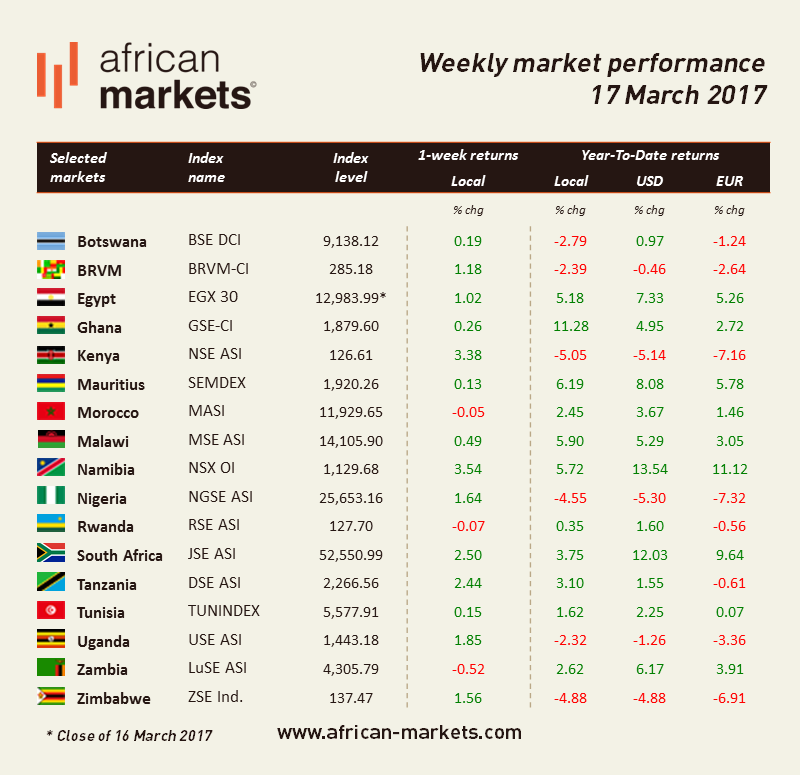

Spring is knocking at the door and even more so on African markets this week. A vast majority of indices closed the week on a positive note and those which did not were really close.

The banking sector has been suffering in Kenya since the President decided to cap commercial lending rates last August. As a consequence, lending rate has significantly decreased in the country with businesses failing to meet their funding needs. According to the central bank, growth in loans to the private sector reached 4.3% in December, falling from 18 % a year earlier. This week, in his final state-of-the-nation address before the August vote, President Kenya talked about rectifying the decline in business lending. For the first time, Equity Group Holdings (NSE:EQTY, RSE:EQTY), one of Kenya’s largest bank, reported a drop in annual profit this week as non-performing loans more than doubled and its loan book shrank 5%. The NSE ASI gained 3.38%.

Maroccan Prime Minister has been made redundant by the King this week following his inability to form a government. Mister Benkirane’s party had won most votes during last elections in October but did not have a majority. Benkirane failed to find an agreement with some parties to create a coalition. The outing of Benkirane should contribute to ease political tensions that partly paralysed the country. The MASI was flattish.

The Fed increased the US policy rate by 25 basis points to a target range of 0.75%-1% p.a. The impact of the rate was a slight increase in the value of the dollar and an expectation of a fall in oil prices. As far as Nigeria is concerned, the rate increase will increase the debt service burden of the country and may reduce Foreign Direct Investment flow into the country. The NGSE ASI gained 1.64%.

South African central bank Governor state this week that it was too early to call the end of its interest rate-increase cycle, even as the risks to inflation have eased since the Monetary Policy Committee’s January meeting. The MPC will announce its next policy move on March 30. Inflation eased to 6.6% in January, the first deceleration in several months, however the Governor thinks that oil and food price still pose risks. The good rains will lead to price of grains coming down but the Governor is concerned about the fact that farmers are restocking their herds and that meat prices remain high which he says does not help. The Governor gave thus a cautious tone to growth expectations for the country as he still sees significant downside. The JSE ASI increased by 2.5%.