")

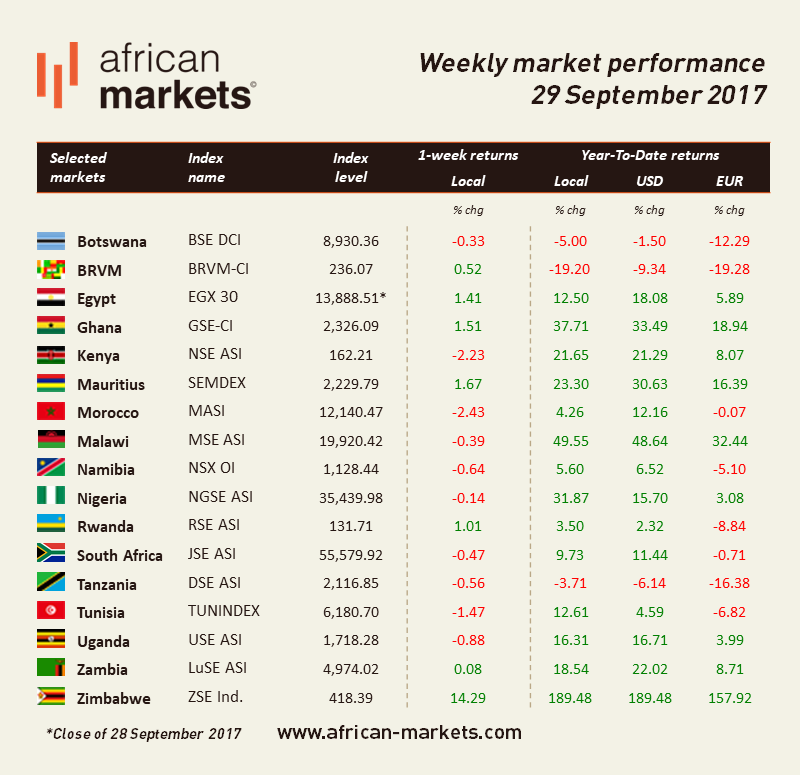

They say October is a symphony of permanence and change and this is quite true for African markets this week. The performance was quite mixed with ZSE keeping its wining spree.

The ZSE is the best performer of this week, adding 14.29%. Afreximbank has made commitment to bailout Zimbabwe with about $1 bn to stabilise the economy. As part of the extension, the Reserve Bank of Zimbabwe (RBZ) and Afreximbank signed a memorandum of understanding for a $600 mn nostro stabilisation facility which is the largest bulk of the fund to be received by the country. The purpose of the $600 million nostro stabilisation facility is to meet the forex requirement for productive foreign payments. There is also a $150 mn letters of credit facility to support the importation of fuel as well as fertilisers and feedstock for the manufacturing of cooking oil. In addition, some of the facilities include $200 mn Afritrades facility to support the banking sector stability which will make interbank lending possible.

According to the bureau of Statistics, Ghana’s GDP grew 9% in the second quarter of 2017 compared to 6.6% in the previous three months. After battling both a commodity and a fiscal crisis Ghana has been able to revamps its economy. The GSE gained 1.51%.

South African index along with other emerging markets came under pressure this week as indications erupted that the US would push through fiscal reforms which attracted investors back to the US markets, supporting the dollar. The rand took a big hit trading at a four-and-a-half-month low. Although a weaker rand is normally good for resources companies since they are paid in dollar for their commodities the support was soft as confidence levels on the JSE at present are low due to political uncertainty around the government's challenge to find money to recapitalise struggling state-owned enterprises. In other news, a Moody’s representative stated this week that the agency feels comfortable with South Africa’s Baa3 with a negative outlook rating. The main concern is the larger shortfall in South African government revenues and an increase in foreign financing of government borrowing in rand which poses a greater risk. The JSE lost 0.47%.

The Central Bank of Egypt's decided to keep interest rates unchanged maintaining overnight deposit at 18.75%, overnight lending at 19.75%, and the rate of the CBE's main operation at 19.25%. Since the MPC's last meeting annual headline inflation fell to 31.9% from 33%. Inflation mostly came from an upward adjustment of regulated prices due to higher electricity tariff. According to the CBE, real GDP growth averaged 4.6% during the second half of 2016/17, growing at the fastest pace since 2009/10. The EGX30 gained 1.41%.

As widely expected, Nigeria’s central bank kept its benchmark interest rate unchanged at 14% on Tuesday. The NGSE lost 0.14%.