")

")

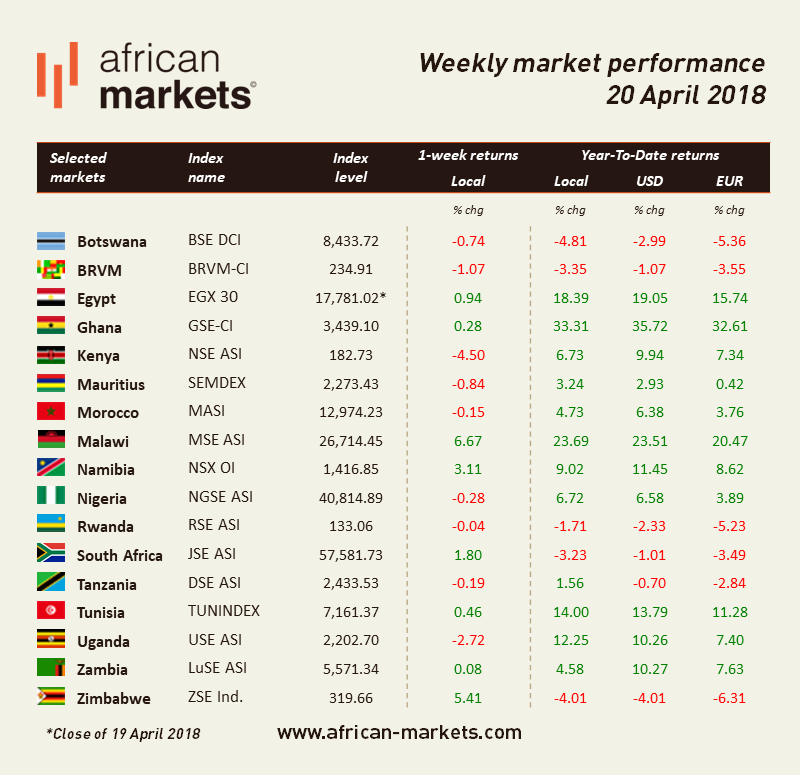

Performance this week was mixed on African markets with very strong performance in Malawi,, Zimbabwe and Namibia and weak performance in Kenya and Uganda.

In its latest World Economic Outlook, IMF has revised its expectations for growth in Zimbabwe for this year from 0.8% in October to 2.4%. The change in leadership with President Emmerson Mnangagwa assuming office is a key basis for this renewed enthusiasm. In addition, The Zimbabwean National Statistics Agency reported that consumer price inflation eased to 2.68% year-on-year in March from 2.98% in February. The ZSE Ind. is up 5.41%.

National Bureau of Statistics reported that Malawi’s consumer price inflation accelerated to 9.9% year on year in March from 7.8% in February. It also indicated that consumer prices fell by 0.9% in March versus February, compared to an increase of 2.1% in February. Nevertheless, the MSE continues to see traction and gained 6.67%.

Ghana saw IMF growth expectations cut by 2.6% to 6.3%. This came as a result of a deceleration in industrial output due to maintenance work at the Jubilee oil field coupled with indications of a smaller cocoa crop this season. The GSE added 0.28%.

Egypt targets an increase in revenues from taxes imposed on tobacco by 7 bn Egyptian pounds ($402 mn) in the 2018-19 draft budget. As part of economic reforms related to a $12 bn IMF programme, the country has been increasing taxes and cutting subsidies to reduce budget deficit. The EGX30 added 0.94%.

Commercial lending rate caps have been the source of debates since their inception in Kenya in 2016. President Uhuru Kenyatta announced this week his intention to modify or suppress the law to address the concerns that have been raised.. The President recognised that the caps have had limited effects on improving access to credit for small and medium enterprises (SMEs) which was their ultimate purpose. The NSE lost 4.50%

IMF also revised its outlook on South Africa’s economic growth for the next 2 years. The IMF now expects GDP to grow 1.5% for 2018 and 1.7% for 2019, compared to previous forecasts of 0.9% and 1.6% respectively. In its outlook, IMF states that business confidence is likely to remain upbeat following change in leadership but economic reforms are key to growth achievement. In the meantime, latest official data showed that the country’s inflation achieved its lowest level in years thanks to the end of the severe drought helped push down food prices. Headline annual consumer inflation slowed to 3.8% in March from 4% in February. The SARB cut its benchmark rate to 6.5% last month but indicated that inflation was at a low point in the present cycle and that it projected consumer prices to increase above 5% in the medium term. The JSE added 1.80%.