")

")

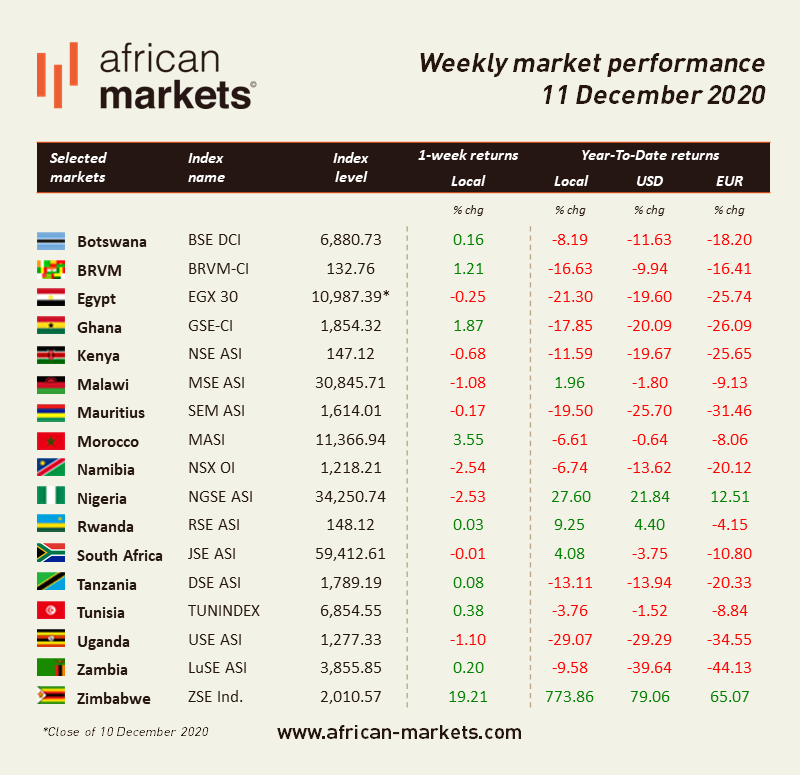

African equities performance was mixed this week with each market reacting to their own set of local factors, while markets in the US, Europe and Asia, were mostly down for the week. Global markets seem to have reacted negatively to unsteady progress toward another covid-19 relief package in the US, unsuccessful negotiations to date on Britain’s trade relationships with the European Union, and were not particularly excited by the ECB extended its bond-buying program.

On the continent, the Zimbabwean market topped the performers list, again, gaining (19.21%) over the week, consolidating thus its leading position year-to-date. Moroccan equities also stood out. They are up 3.55% this week. The North-African market has been up for the last 8 trading sessions and its benchmark index jumped 2.45% on Friday on news Morocco has become the latest Arab League country to agree to normalise relations with Israel in a deal brokered with the US help. As part of the deal, the US has agreed to recognise Morocco's claim over the disputed Western Sahara region. Besides, the market digested the successful placement of a 3-part $3bn international bond by the Kingdom earlier in the week. The bond, which was four times oversubscribed, is divided into securities of 7 years, 12 and 30 years each worth 750 million dollars, 1 billion dollars and 1.25 billion dollars.

On the other hand, the Lagos market saw its benchmark index lose 2.53% this week. The index was down every single day as investors took their profits. Some analysts expect the market to remain bearish in the near-term given what they described as a “state of overbought”. Investors are expected to remain cautious about investing in the absence of “any major positive catalyst”. Besides, on the macro side, tensions on the FX market are not reassuring.

The overall situation year-to-date has not changed much. Most African markets remain down so far this year and have not recovered from the sell-off in March, with the notable exceptions of Nigeria and Zimbabwe. Both markets are significantly up this year both in local and foreign currencies. Note that the Johannesburg Stock Exchange is up 4% YTD in local currency. It might even end the year in positive territory in dollar terms.

fines 9 companies N76.8 million for default filings of annual financial statements")