")

")

Improving economy and slowing inflation are raising expectations for rate cuts in several African countries. We expected Nigeria and Kenya to follow Ghana’s lead and it is now a done deal in Kenya since the central bank just cut the benchmark rate.

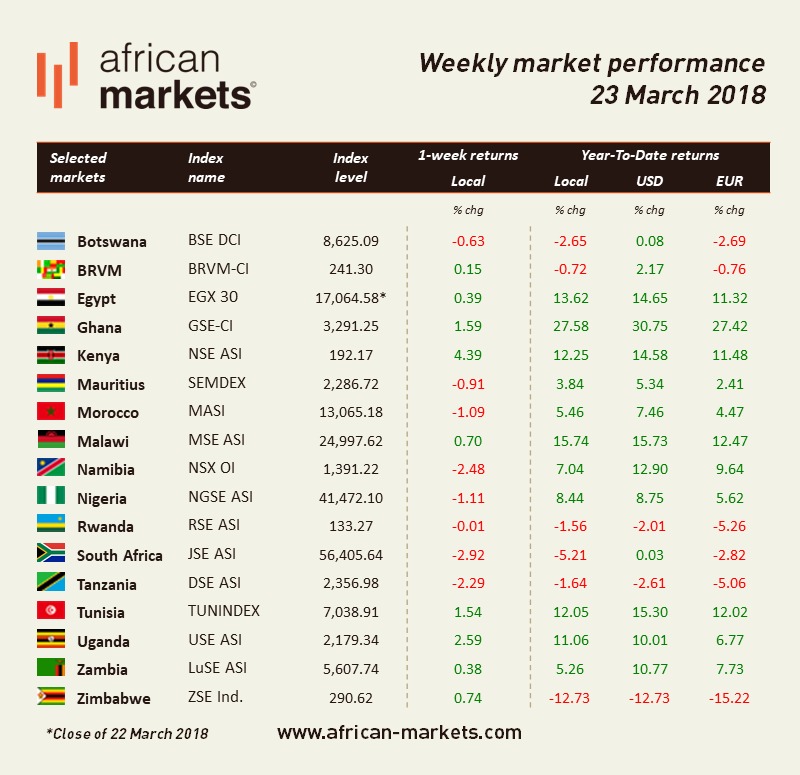

The NSE added 4.39%. Kenya’s central bank cut its benchmark lending rate by 50 basis points to 9.5% on Monday. The bank’s decision is based on moderating inflation and improving growth prospects as the economic output is below its potential level. The rate cut has increased anticipation for a removal or at least a reduction of the commercial rate caps which have hurt Kenya’s economy since introduced in 2016.

Moody’s kept its rating on South Africa’s local- and foreign-currency assessments at Baa3, unchanged from its November’s assessment. However, the outlook was changed to stable from negative. The agency cites new political leadership as the argument which supported its decision. This provides some relief although actual reforms will need to take place to give more confidence about South Africa’s rating. In other news, Naspers sold a 2% stake in Tecent for $9.8bn in order to strengthen its finances and invest over time in its classifieds, online food delivery and fintech businesses globally. Naspers has indicated that it had no plans to reduce its holding further. The JSE lost 2.92% as Naspers weighed on the index.

Bank of Uganda has reported that Uganda’s national debt has soared in the last 3 years to more than 50% of GDP. The bank warns that the increasing cost of debt could hamper economic growth because of reduced public investment. Roughly two-thirds of the debt is external which the bank says poses a default risk in case of exchange rate volatility and slow growth in exports. Growth has been decelerating in Uganda following poor agricultural output, weak exports and corruption. The USE gained 2.59%.

Rwandan Finance minister expects the country’s economy to grow by 7.2% this year. Growth should be supported by the services sector and a rebound in construction. This is in line with IMF expectations of between 7-8% growth. The RSE lost 0.01%.

Morocco’s central bank kept benchmark interest rate 2.25%. Bank al-Maghrib said inflation was expected to reach 1.8% on average in 2018 and to fall to 1.5% in 2019. GDP growth is expected to reach 3.3% this year and 3.5% in 2019. The well-received new more flexible exchange rate system introduced in January as well as improving economy and moderating inflation supported the bank’s decision. The MASI lost 1.09%.

S&P reaffirmed Ghana’s B-/B ratings this week and remained positive regarding its outlook. The agency anticipates strong real economic growth for the country over a period until 2021 due to increasing oil production. The GSE added 1.59%.