")

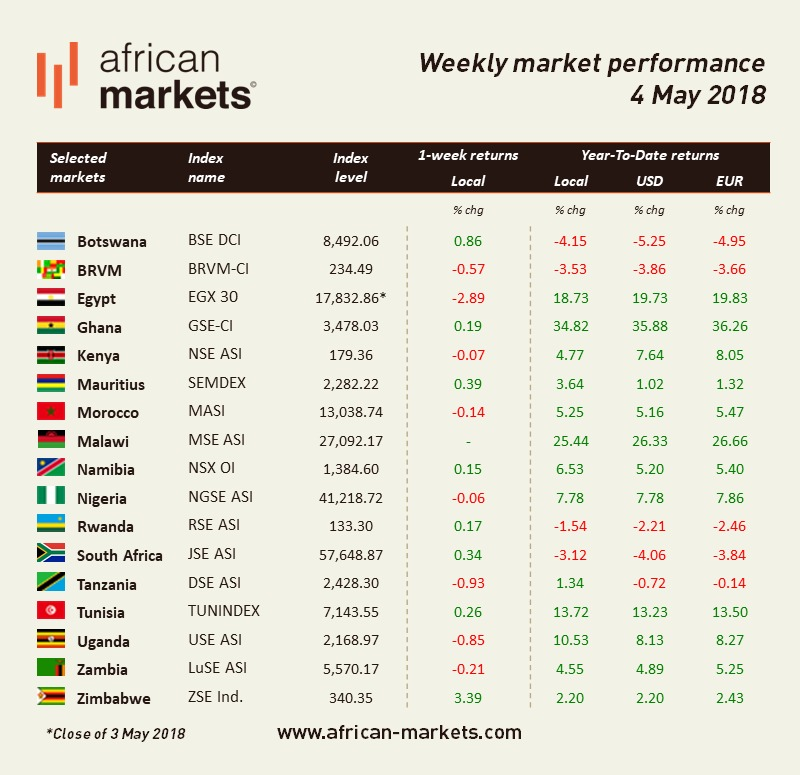

It is another week of mixed performance on African markets. Egypt is back on red territory and Zimbabwe continues to surprise positively.

Headline inflation lowered further in April to 1.8% from the 2.0% for the year ended March 2018. The drop was mainly due to the deceleration in annual food crop inflation which recorded -2.1% compared to -1.7% for the year ended March 2018. This was due to a reduction in prices of fruit with annual fruit inflation slowing down to -8% from the -5.1% over the same period. Annual core inflation also dropped to 1.6% compared to 1.7% for the year ended March 2018. A fall in the price of sugar and bread and cereals drove the decrease. Sugar inflation dropped to -20.9% for the year ended April 2018 from -14.7% in March, while bread and cereals inflation decreased to -5.3% from -0.4%. The USE lost 0.85%.

In South Africa, local economic data provided some support to the JSE this week. The ABSA Manufacturing PMI beat consensus estimates. April number jumped to 50.9, which was better than the forecast 48 and higher than the prior recording of 46.9. Year-on-year numbers for Naamsa vehicle sales also surprised to the upside at 3.6%, versus the forecasted 2.0%. The JSE added 0.34%.

The Bank of Ghana in consultation with the Ghana Association of Bankers reconstituted a Working Group to review the existing Base Rate model and develop a new framework for base rate determination. The ‘Base Rate’ emanating from this model is now a Reference Rate rather than a Minimum Lending Rate for all banks as was the case with the previous model. Ghana reference rate for May pegged at 16.74%. The GSE added 0.19%.

Kenya’s Treasury cut its outstanding overdraft facility at the Central Bank of Kenya (CBK) by 75% as healthy inflows from government securities ease cash flow worries. The government makes use of the facility to plug short-term cash holes, paying interest at the prevailing Central Bank Rate (currently at 9.5%). The drop in the overdraft facility implies that government cash flows have improved. The NSE lost 0.07%.

Tunisia’s annual inflation rate rose to 7.7 percent in April from 7.6 percent in March. The central bank increased its key interest rate to 5.75% from 5% last March to fight inflation. According to the state statistics, the food and drink price index rose 8.9% in April from a year earlier while the price of vegetables rose 23.8%. TUNINDEX added 0.26%.

According to the President, Malawi’s economy will grow by 6% in 2019 from a 4% expansion expected in 2018. Mutharika stated that after three years of battling the devastation of Cashgate, drought and floods, the economy has turned around.