")

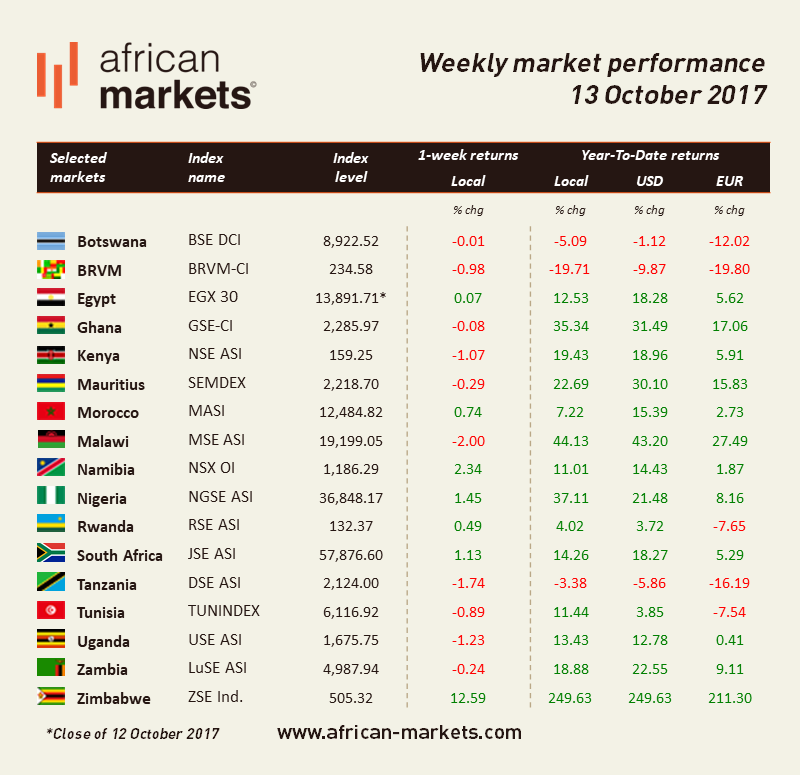

The mixed trends continued this week on African markets with half of the indices under our coverage closing on negative territories. And the answer is yes, the ZSE is still this week’s best performer. Something tells me this will be the case for a while.

In Kenya, opposition leader Odinga pulled out of the repeat presidential election expected to be held on 26th October. Odinga stated that the repeat election should be cancelled and a new election held after the election board has carried out reforms. Political uncertainty has hit the Kenyan stock market and should continue to do so at least until the 26th October should the date of the repeat election be maintained. The NSE lost 1.07%.

According to the Rwandan’s National Bureau of Statistics, inflation grew to 3.8%in September from 3.2% the month before mainly due to food and non-alcoholic beverages, housing, water, gas and electricity. The RSE gained 0.49%.

Inflation also rose in Tanzania due to increases in food prices. Inflation rate reached 5.3% in September from 5% a month earlier. The food and non-alcoholic beverages inflation rate increased to 9.3% in September from 8.6%. The DSE lost 1.74%.

South African central bank governor Naidoo stated this week that credit downgrades risk is quite significant. According to Naidoo South Africa’s local currency rating could cost $8 to $12 bn in lost investment. Both Fitch and S&P downgraded South Africa’s foreign-currency rating to speculative grade or junk last March. Naidoo stated that weak growth is mainly due to domestic factors and projected the economy to grow 0.6% to 0.7% and inflation to remain within the target range 3%-6% for the next two years. The JSE gained 1.13%.

The IMF stated that Zambia’s public debt has been growing unsustainably. The rise of the public debt has crowded out lending to the private sector and in turn increased the weakness of the economy. External debt increase has put Zambia at high risk of debt distress. Despite easing of the government’s financing constraint thanks to rising involvement of foreign investors in the stock market, increased participation to has made the economy more vulnerable to swings in market sentiments and capital flow reversals. The IMF expects the economy to grow 4% in 2017 lower than government’s expectations of 4.3%. This is mainly due to delayed fiscal adjustment and unfavourable weather conditions affecting hydro power generation and agricultural output as well as tighter global financial conditions and volatility in the world copper price. The LuSE lost 0.24%.

Egyptian finance minister announced that the country intends to re-enter a $2 bn financing agreement with international banks while also putting alternative sources of financing in place such as issuing dollar-denominated Eurobonds. The goal is to finance the deficit and repay foreign debt. In 1Q18 the country will likely sell $4 bn of dollar-denominated bonds and €1.5 bn of euro-denominated debt. The finance minister also stated that the IMF may provide another $4 bn before June. The EGX30 gained 0.07%.