")

")

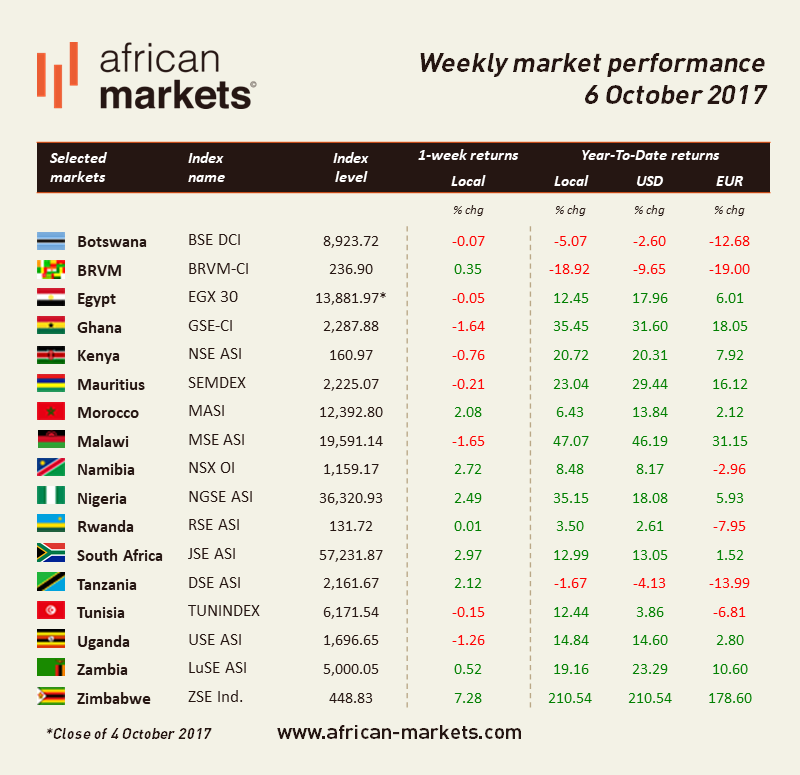

The first week of October started in a positive fashion with 9 out of the 17 indices under coverage evolving in green territories. The ZSE continues to be the outlier marking the strongest performance this week.

The JSE rose 2.97%. According to the South African Reserve Bank (SARB), the economy is growing much less than anticipated and is unlikely to reach 2% annual expansion in the short term because of political and policy uncertainty. The bank expects growth to barely exceed 1.5% by 2019, well below the government’s long-term target of 5%. The bank stated that bigger shortfalls in government revenues increased the likelihood of deeper credit rating downgrades which supported its decision to maintain lending rates unchanged during its last meeting in September. Weak economic outlook CPI expectations close to the upper-end of the range provide some scope for lower interest rates. In other news, Vodacom share price plunged 8.5% following the launch of an antitrust probe into a contract with the National Treasury that might involve an abuse of market dominance.

The NGSE added 2.49%. In Nigeria, the senate has launched an investigation into alleged financial mismanagement at the state-owned oil company. The managing director of the Nigerian National Petroleum Corporation is being accused of awarding contracts worth more than $26bn without due process.

The NSE lost 0.76%. Kenya’s opposition has not reached an agreement yet on the way the presidential election will be conducted this month. The opposition has detailed several measures it wants to see before proceeding to the re-run of the election. A change from staff and electronic systems are among the main requests. Uncertainty regarding the presidential election has been weighing on sentiment for some time now.

Last month, Ghanaian regulators raised the minimum capital requirement for banks from 120 mn cedis to 400 mn cedis with banks needing to meet these new rules by year-end. According to Ecobank, meeting this new requirement within the given timeline will be difficult and may trigger consolidation in the sector. The GSE lost 1.64%.

In Zimbabwe, the cash shortage is stronger than ever spurring an increase in the price of goods and in a vicious circle is limiting supplies. According to the Statistics bureau, consumer prices increased by 0.1% year-on-year. The ZSE gained 7.28%.

The Central Bank of Egypt has decided to lift the cash reserve ratio for banks to 14% from 10% starting from 10 October 2017. The goal is to reduce inflation rates to 17% by 2018 as an alternative solution for boosting interest rates to face the growth of cash liquidity. The jury is out on whether the decision will reach its intended purpose because of the current consecutive gap between inflation rates and deposit interest rates. The EGX30 lost 0.05%.