")

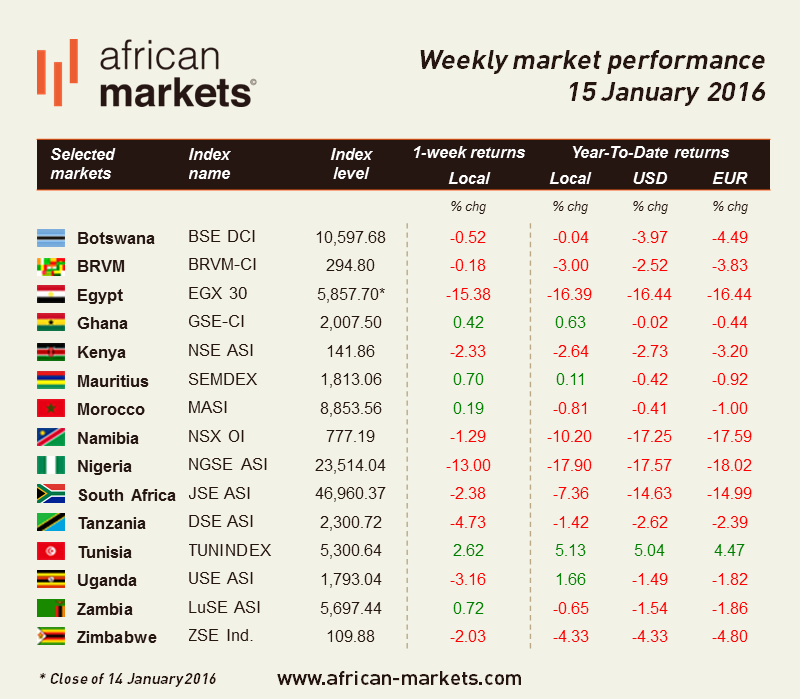

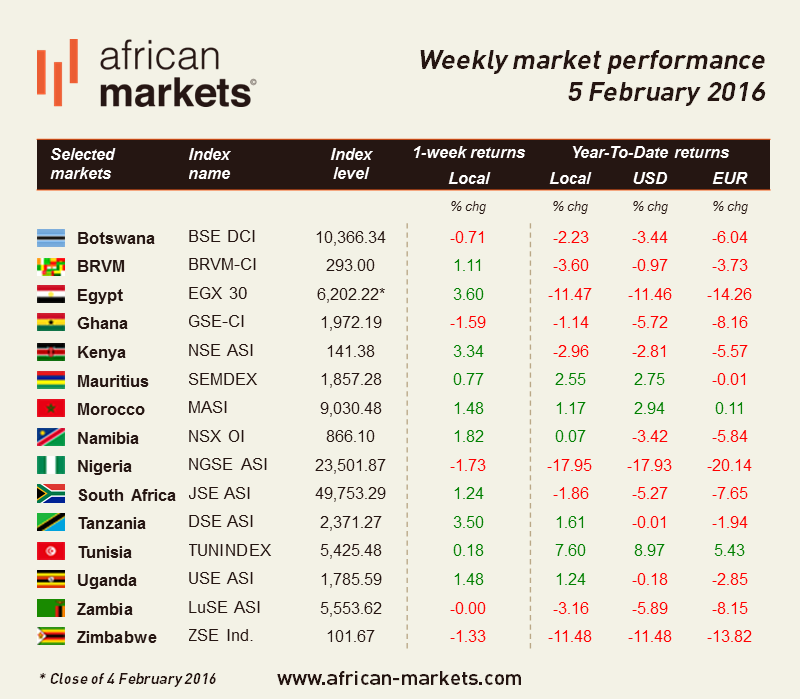

African markets ended the first week of February with the majority of indices sitting on the green zone. The week was marked by a mining rally driven by a sliding dollar making commodities attractive alternative investments despite fundamentals basically unchanged and prone to remain that way for some time. Contributing to the new positive sentiment were speculations that the Chinese economy would reenergise as the country set its growth target at 7% for 2016, higher than most consensus expectations.