")

")

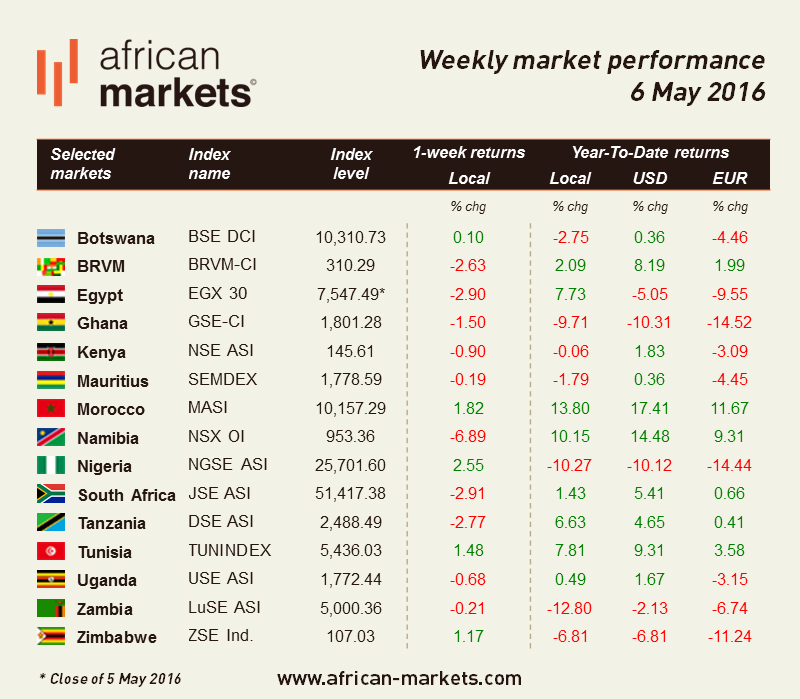

The party theme must certainly have been red this week on African markets as most of them adopted the look perfectly. African stocks experienced the longest losing trend since December, as markets held their breath on concerns the United States April payroll report could support the idea that the US economy is strong enough to justify higher interest rates.

In parallel, emerging-market currencies underwent their biggest five-day drop in four months following statements from Fed officials this week that the central bank may hike interest rates before the end of the first half. The general consensus was that the Fed would not increase rates at its next meeting in July, but those statements gave the dollar another boost. Markets had to wait the end of the week to find some relief as the Bureau of Labor Statistics reported that domestic nonfarm payrolls increased by 160,000 in April, considerably below a gain of 209,000 in March, its lowest level in seven months. Nevertheless, the unemployment rate remained unchanged at 5.0%, while average hourly earnings increased by 0.3%, in line with consensus estimates. At the cost of repetition, interest rates hike may lead to capital outflow from African markets to the US.

Lasting negative sentiment on global markets pushed share prices on the JSE ASI lower. The index was lower on four of the five days this week and fell by 2.91% for the week. Moody’s announced Friday that it was maintaining South Africa’s investment-grade rating while assigning a negative outlook to it. The agency said that it had now concluded a ratings review it launched on March 8.There had been a lot of concerns that the country’s government debt would be downgraded to junk this year. The confirmation of the rating reflects Moody’s view that an inflection point could be seen after years of falling growth and should be reassuring for investors. Moreover, Barclays started its Africa exit after it sold shares equivalent to a 12.2% stake in South Africa-based Barclays Africa Group. The UK firm said it has sold the first tranche of 103.6m ordinary shares for USD 876m to undisclosed investors. The exit process should be completed in three years.

Head to head with the JSE ASI, the EGX30 experienced significant losses and decreased by 2.90%. Trading on the Egyptian Stock Exchange was surrounded by caution following low liquidity. The Egyptian bourse signed cross-listing agreement with Bahrain stock exchanges. Cleopatra Hospital, an Egyptian hospital group owned by Abraaj Group, announced its intention to attract new capital investments by offering 40m shares on the Egyptian Exchange, the 40m shares are 25% of the company’s total capital listed on the EGX.

USE ASI was down 0.68%. The Ugandan government has lost about USD 28 mn in taxes and export earnings due to a production shortfall by Kakira Sugar Works, the country’s biggest sugar producer.

NGSE ASI is up 2.55% this week despite Nigeria’s long-term issuer ratings being downgraded to B1 from Ba3 by Moody’s which nevertheless assigned a stable outlook. Also, according to the National Bureau of Statistics, investment inflows drops to nine-year low at NGN 140bn. It seems this did not shadow the Nigerian market’s excitement following the decision to retain Nigeria in the MSCI which led to an upbeat market sentiment.

ZSE Ind. closed the week up 1.17% as investors seem to play some value despite the tougher operating environment the country is experiencing since last year.