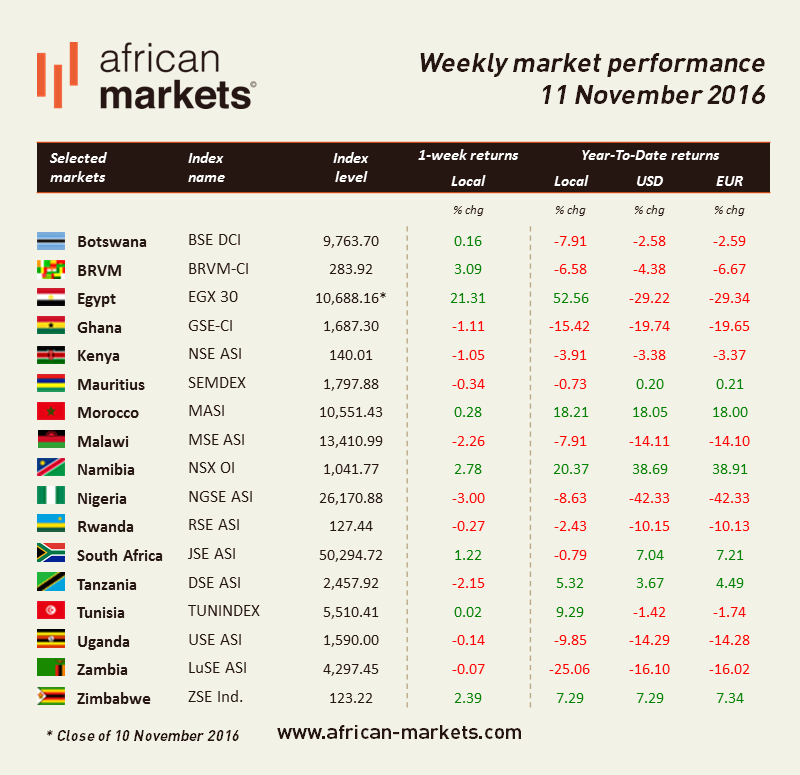

It may seems as if this edition is focused on Nigeria, and you are right, a lot of movement on the Nigerian stock market took place this week.

Select your language

")

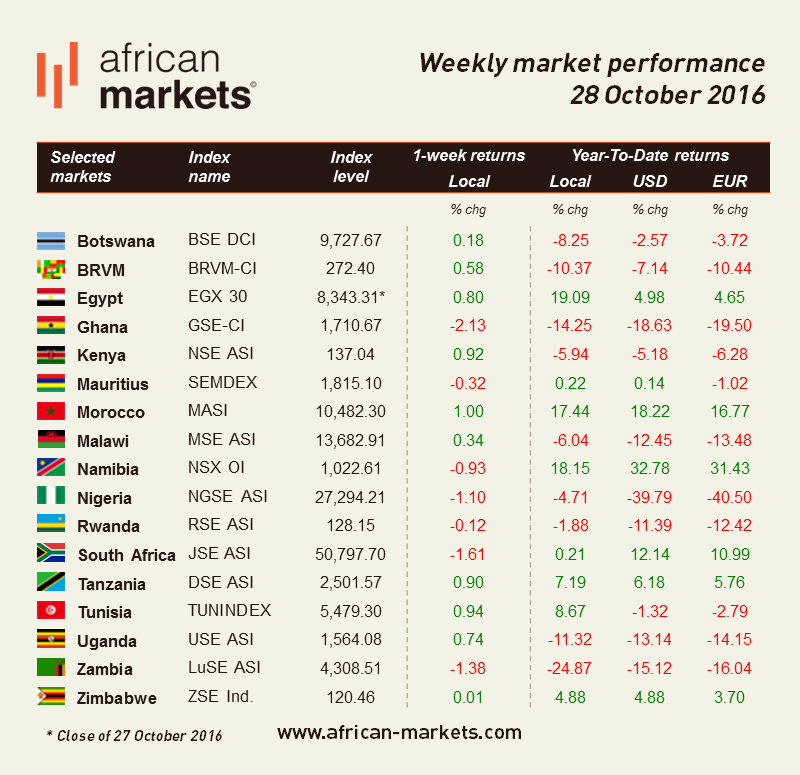

It may seems as if this edition is focused on Nigeria, and you are right, a lot of movement on the Nigerian stock market took place this week.

The United States elected their new President this week, globally markets reacted pretty well or not as bad as they were expected. What about African markets? During his campaign, Trump has been highly vocal about his willingness to file trade cases against China. Should this materialise, further contraction of the Chinese economy would be negative for African economies that are dependent on export to China. However, given the size of the US debt that China holds (~$1.3T), and potential retaliation, it seems difficult to enforce and not necessarily a sensible step to take.

The EGX30 is the top performer of the week, gaining 5.60%. Excitement gain the Egyptian market this week as the Central Bank of Egypt finally decided to allow the Egyptian pound to float and increase interest rates by three percentage points. The devaluation of the pound will put the currency on par to its value on the black market. The benchmark strengthened as a result as the move brought the country closer to securing a $12bn loan by the IMF. Dollar shortage means that investors will still face capital controls preventing them to repatriate profits.

In its bi-yearly report IMF cut its 2017 growth outlook for sub-Saharan Africa to 1.4% from 3% growth expected earlier because of commodity-exporting countries struggling with weak demand. Sub-Saharan Africa is witnessing its lowest growth in 20 years however some countries still expect to expand by 4% or more.

Page 30 of 41

| BRVM-CI | 290.79 | +0.55% | 11/04 |

| BSE DCI | 10,113.04 | - | 11/04 |

| DSE ASI | 2,282.58 | +0.19% | 11/04 |

| EGX 30 | 30,810.70 | +2.43% | 10/04 |

| GSE-CI | 6,100.93 | +0.02% | 11/04 |

| JSE ASI | 90,149.69 | +1.41% | 19/03 |

| LuSE ASI | 16,408.20 | +0.02% | 10/04 |

| MASI | 16,070.49 | -1.87% | 11/04 |

| MSE ASI | 294,562.18 | -0.62% | 11/04 |

| NGX ASI | 104,563.34 | -0.21% | 11/04 |

| NSE ASI | 126.78 | +0.81% | 11/04 |

| NSX OI | 1,792.80 | +0.64% | 19/03 |

| RSE ASI | 148.96 | - | 11/04 |

| SEM ASI | 2,118.07 | -0.19% | 11/04 |

| TUNINDEX | 10,877.06 | -0.05% | 19/03 |

| USE ASI | 1,262.37 | -2.50% | 11/04 |

| ZSE ASI | 200.42 | -0.96% | 11/04 |